Van Stuijvenberg Financial Services is very proud to announce that Altis – NNIP’s independent manager selection & monitoring team – has chosen Van Stuijvenberg Financial Services to provide them with LDI tooling. The tooling will be used to monitor LDI solutions that are in place with NNIP’s fiduciary clients. NNIP already has elaborate systems in place and by adding an external, independent LDI toolkit NNIP adds an extra layer of control. Van Stuijvenberg Financial Services looks forward to the implementation and is eager to add value and efficiency to the monitoring process.

NNIP – Altis | Van Stuijvenberg Financial Services

Posted in Uncategorized

Comments Off on NNIP – Altis | Van Stuijvenberg Financial Services

Nordic Unrated & Rated Credits (NURC) from the perspective of a typical Dutch Pension Fund…

On the 25th of May 2022 the Finnish asset manager EVLI presented at the FFH annual institutional investor event making the case for Nordic Unrated & Rated Credits (NURC). Van Stuijvenberg Financial Services (VSFS) looked into this asset class from the perspective of a typical Dutch pension fund. Below you find a quick overview of this analysis.

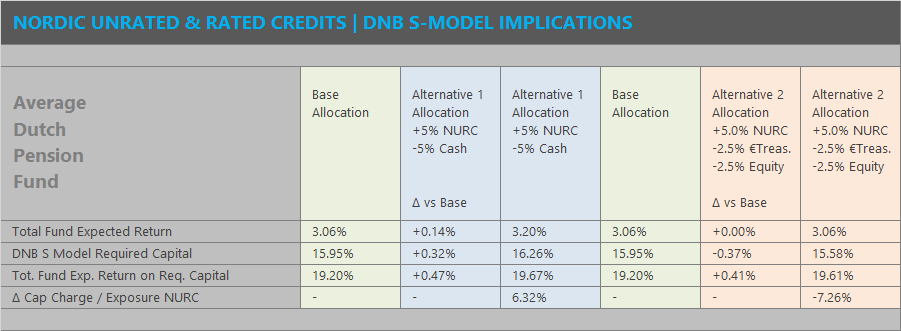

Although the Dutch are moving towards a new pension system the current regulatory framework still is important. In the current regulatory framework an allocation to NURC would impact the pension fund’s required capital (solvency buffers) as calculated by the so called DNB S-Model. Some pension funds have a high solvency ratio and are not constrained by the DNB S-Model while for others the buffer requirements are a true constraint. For the latter group the impact on required capital is an important variable when making the decision to invest in NURC. Basically – like an insurance company – these pension funds try to optimize the return on required capital.

As a first step VSFS looked into the regulatory repercussions of allocating to NURC. Analyzing the impact from a regulatory perspective VSFS considered 2 alternatives for implementing a NURC allocation:

- Fund a 5% allocation to NURC from cash.

- Fund a 5% allocation to NURC from € treasuries and equities – in a 50/50 ratio – while keeping the liabilities hedge ratio constant at 60%.

In alternative 1 – funding from cash – the total expected return for the typical pension fund goes up from 3.06% to 3.20%. The required capital though rises too from 15.95% to 16.26%. Because the total fund expected return rises sharper than required capital the return on required capital increases from 19.20% to 19.67%. This makes that – from a regulatory perspective – it can be interesting to invest in NURC (funded by cash) since doing so improves the return on required capital.

Some pension funds might be extra constrained and therefore not eligible to raise the DNB S-Model required capital. When making investment decisions they must always make sure required capital does not increase. For these pension funds alternative 2 – funding from € treasuries and equities – is a possibility. In this alternative the expected return stays at 3.06% while required capital goes down to 15.58% implementing an increase in the return on required capital to 19.61%.

Looking at the 2 alternatives above VSFS concludes that NURC is an intersting asset class from a regulatory perspective. One can increase the return on required capital by investing in NURC and depending on the pension fund’s situation and appetite one can choose to increase or decrease capital requirements.

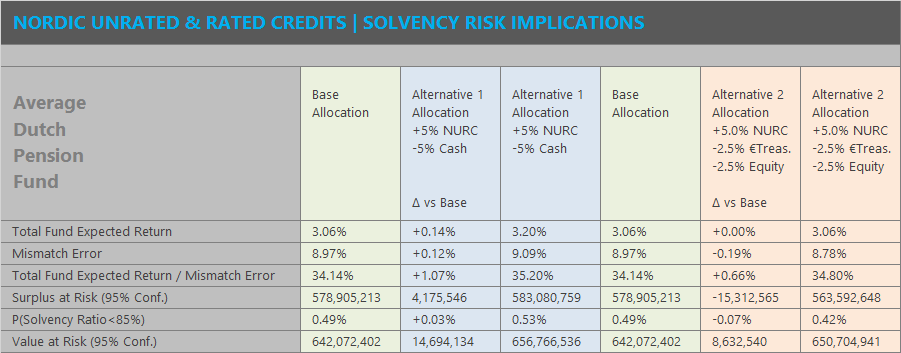

So far for the regulatory point of view… As a next step VSFS looked into the impact on solvency risk and the expected return / solvency risk ratio. Here solvency risk is measured by the mismatch error which is the tracking error of the total pension fund’s assets vs it’s liabilities priced at the so called Dutch UFR discount curve. Also from this perspective allocating to NURC can be fruitful.

Looking at alternative 1 again – funding the NURC allocation from cash – the expected return goes up from 3.06% to 3.20%. The mismatch error increases from 8.97% to 9.09%. Since the expected return shows a sharper increase than the mismatch error the expected return / mismatch error ratio goes up from 34.14% to 35.20%. Here the 5% allocation to NURC funded from cash improves the expected return / solvency risk ratio making it a sensible, effcient decision.

As discussed alternative 1 might not be possible for all pension funds because of regulation. Alternative 2 – funding NURC from € treasuries and equities – is an option for all pension funds and keeps the total fund expected return equal while reducing mismatch error. This results the expected return / mismatch error ratio to increase to 34.80%. Here again allocating to NURC is beneficial from a total return / solvency risk perspective.

Based on this case study VSFS concluded that for a Dutch pension fund it’s certainly worthwhile to consider allocating to NURC. On the regulatory side one can improve the return / required capital ratio while from a solvency risk point of view one can improve the return / solvency risk ratio. The tables below show the key findings for a typical Dutch pension fund. For most pension funds the findings will be similar but of course depend on it’s specific assets and liabilities.

If you are interested in an custom analysis based on your pension fund’s situation please reach out to:

- Jan Willem van Stuijvenberg at jw@van-stuijvenberg.com

- Richard Crombach at richard.crombach@tcp-global.com

This short article was first posted on July 12th 2022 at van-stuijvenberg.com

Posted in Uncategorized

Comments Off on Nordic Unrated & Rated Credits (NURC) from the perspective of a typical Dutch Pension Fund…

Financial Investigator Roundtable LDI & Balance Sheet Management

In February 2021 Financial Investigator hosted a LDI & Balance Sheet Management Roundtable. Jan Willem van Stuijvenberg was one of the participants and very much enjoyed the discussions on this always interesting and evolving topic.

In February 2021 Financial Investigator hosted a LDI & Balance Sheet Management Roundtable. Jan Willem van Stuijvenberg was one of the participants and very much enjoyed the discussions on this always interesting and evolving topic.

The questions covered at the roundtable:

- Should balance sheet management and LDI be provided by one party?

- Should one hedge currency risk inside the LDI mandate or at a total fund level?

- What are the pros and cons of a ‘fund for one’ vs a ‘segregated account’?

- Does it pay out to be active in LDI using government bonds, SSA’s etc.?

- What possibilities are there to incorporate green investing / ESG in LDI?

- The scope of instruments that are used in LDI is widening. How to cope with this?

- For central clearing are pension funds willing to expand towards LCH?

- How does one cope with the increasing demand for cash collateral and the possible drag on performance?

- How will the ‘New Pension Contract’ impact LDI and is anticipation needed?

- In the ‘New Pension Contract’ one will work with age groups. Is it truly logical to increase the rates hedge with age?

- Over 2021 / 2024 the regulatory UFR discount curve will change. How to cope with these changes in relation to the upcoming ‘New Pension Contract’?

- Should (long) government bonds be a natural part of an LDI portfolio?

- What is your outlook on the shape and level of the swap curve?

Download Article

Posted in Uncategorized

Comments Off on Financial Investigator Roundtable LDI & Balance Sheet Management

Mercer and Van Stuijvenberg Financial Services prolongate cooperation.

Jan Willem van Stuijvenberg

Karin Roeloffs

Mercer and Van Stuijvenberg Financial Services prolong their cooperation on pensionfund balance sheet management and interest rate hedging solutions for 3 years. The cooperation started in 2006 when Mercer acquired licences for the risk and LDI tools of van Stuijvenberg Financial Services. Together they further developed the tools and for the future the ongoing development will play a key role.

Over the last 11 years Mercer advised more than 40 pensionfunds with total assets over €150 billion. Risk and LDI tools were essential in doing so. The ongoing development kept us up to par with the continuously changing environment. The continuation of this joint development is an important part of the contract that was signed. To stress the structural relationship the contract has a maturity of 3 years with the intention to prolong.

A solid setup and an effective monitoring of the interest rate hedge is key for pensionfunds.

In the prolonged cooperation van Stuijvenberg Financial Services will be responsible for the ongoing development of tooling. Van Stuijvenberg Financial Services will also support the Mercer consultants. The focus for this support will be on risk and LDI issues.

Karin Roeloffs, the head of Mercer Investments Netherlands: “For Dutch pensionfunds a solid setup and an effective monitoring of the interest rate hedge is key. We have been working on risk and LDI with van Stuijvenberg Financial Services for eleven years now. This cooperation has added clear value for our clients and that is what we will continue to do for the years to come. Van Stuijvenberg Financial Services has elaborate knowledge and experience in LDI and has proven to develop very useful risk and LDI applications.”

Jan Willem van Stuijvenberg, owner and founder of van Stuijvenberg Financial Services: “Mercer is a very professional and pleasant party to work with. We work together for 11 years now and achieved a lot. Working with the Mercer consultants is very valuable to me. The feedback and suggestions they give help me making better applications. I think that supporting the consultants on risk and LDI while at the same time developing and improving the applications they use is very efficient. I look forward to add value and work with Mercer for another 3 years.”

About Mercer

Mercer is a global leading provider of advisory services on Health, Wealth en Career. The Mercer consultants support their clients on complex issues. These can be related to working conditions and benefits, human capital, health plans and insurance, social security and pensions. In 43 countries over 20,000 people work for Mercer. Mercer is wholly owned subsidiary of MMC. Also Marsh en Oliver Wyman are part of MMC.

Posted in Uncategorized

Comments Off on Mercer and Van Stuijvenberg Financial Services prolongate cooperation.